Back home again last weekend, which was great.

Mum loves TV shows about home renovations1. Every time I’m back there seems to be a constant stream of shows about property development on the telly.

Whether it is Kirsty and Phil, George Clarke or Homes Under The Hammer - she loves it all.

I’m not entirely sure why, although I’m pretty convinced that it is because it gives her (and I) licence to judge other peoples’ appalling interior design choices.

I am a total layman with this stuff - but from what I can tell the process of building or renovating a house is a pretty exact science.

Get your measurements right, execute correctly and you’ll end up with (or pretty darn close to) the intended result.

Investing, and financial planning in general, are not like that. X+Y does not always equal Z, and that is one of the reasons why people can become frustrated as investors. “I’ve done all the right things, why am I not getting the result I deserve” - time to blame the Bank of England/the government/anyone who is on hand.

One approach to building a financial plan relies on making assumptions on what future market returns, rates of inflation, interest rates etc. may be in future. Anything that is a “known unknown” essentially.

Any plan is better than no plan, but the sad reality is that such a plan will be out of date the day it is written. One of the reasons for this is that stock market returns do not neatly and politely follow their long term averages year in and year out.

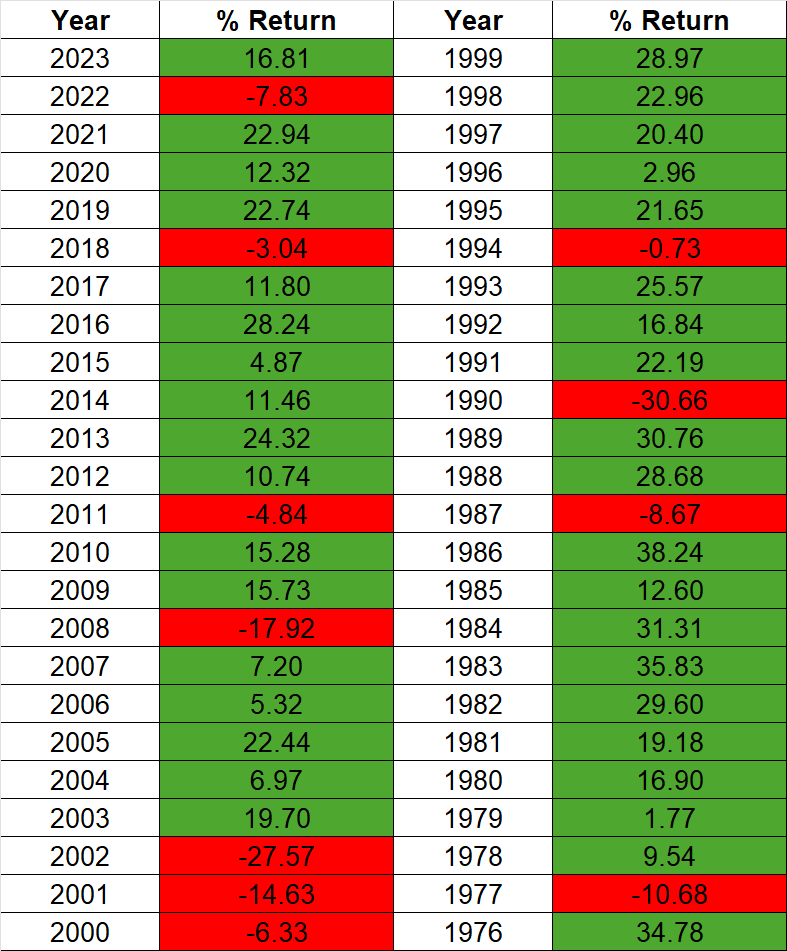

To illustrate this, the below table shows calendar year returns for the global stock market2 since 1976.

During this period, the average calendar year return for the global market was a hair over 12%3.

But what we notice from the above table is just how rarely the market generated this average return - or even close to it.

The market generated a return within 10% of the 12% average in only 4 of the 48 years shown. In only 5 of the 48 years shown did it generate a return within 20% of the 12% average.

The “average” then covers up a huge amount of variability. Most good years, are great years. Stripping out the down years from the numbers above, the average return during “green” years is 19.2% which is obviously incredible.

But of course, in practice, we can’t strip out the bad years. In fact, the bad years are needed in order to have such strong returns during the good times.

If history is any guide, capital markets work really well most of the time, until they don’t. The trend is in the right direction overall, but you need to walk through the fire every once in a while.

I suppose, in this way at least, investing mirrors life in general.

Relying too heavily on average returns also ignores that there can be a huge difference in outcomes, even for two similar investors investing in similar strategies, depending on when they invest.

The below chart shows an (anonymised) screengrab from a financial plan that I put together for some clients recently.

What you are looking at are projections for these clients’ financial futures, based on hundreds of actual past scenarios incorporating over a hundred years of market and economic data.

As you can see, there is a huge dispersion of outcomes based on which “journey” the clients end up eventually going on.

The best case scenario in the dataset above has the clients dying in 39 years’ time with a casual £31.65 million in the bank. The worst case scenario has them running out of money in 20 years4.

Unless something historically unprecedented happens, their outcome will be between those two bounds. The truth is very likely to be in there somewhere.

You might think this is so vague as to not be all that helpful, but I find that using this methodology of planning underlines to the client that this process is to a large extent, art rather than science. We aren’t building a house here.

In chemistry, the term “malleability” refers to a metal’s ability to be manipulated into a new shape without bending or breaking.

The value of malleable metals like gold, copper, tin and aluminium lies in their ability to adapted for purpose without losing their structural integrity. Because of this characteristic, malleable metals enjoy infinitely more commercial use than their non-malleable equivalents.

I like thinking of a financial plan in terms of malleability. While we must have a strong plan in place, grounded in historical data, it is equally important to acknowledge that this will need to be flexed to react to changes in circumstances - both internal and external.

Having this characteristic in place ensures that the plan has as much practical utility as possible.

Have a great weekend.

None of the above is intended to constitute advice to an specific individual. Past performance is not indicative of future returns.

And about haunted houses too strangely enough.

I have used the MSCI World Index this time around, which isn’t my preferred method (I prefer the MSCI All Country World Index as it includes Emerging Markets) but MSCI World has a longer dataset available and is “good enough”.

Most commentators will quote an average long term annual return of around 10% for global equity markets based on what the S&P 500 has done over the past 100 years or so - so a little bit less Either way, my point still stands.

For those of you that are interested, the best case scenario in this case saw the clients investing in January 1921. The worst case had the clients investing in August 1968 - the early years of investment running through the 70’s, a period of very high inflation and not great market returns.