The Perfect Investment Strategy

Is the one you can stick with.

Two things.

I deliberately don’t do weekly recommendations because who cares, but if you haven’t seen ‘Adolescence’ on Netflix you really must. Equal parts captivating and challenging. It’s as close to a masterpiece as TV gets IMO.

On a somewhat different note, this week’s effort is inspired by this brilliant post on LinkedIn by Eric Nelson CFA. It was refreshing to see something so thoughtful on what has largely become a desert of selfies and AI generated drivel.

Anyway, let’s get to it.

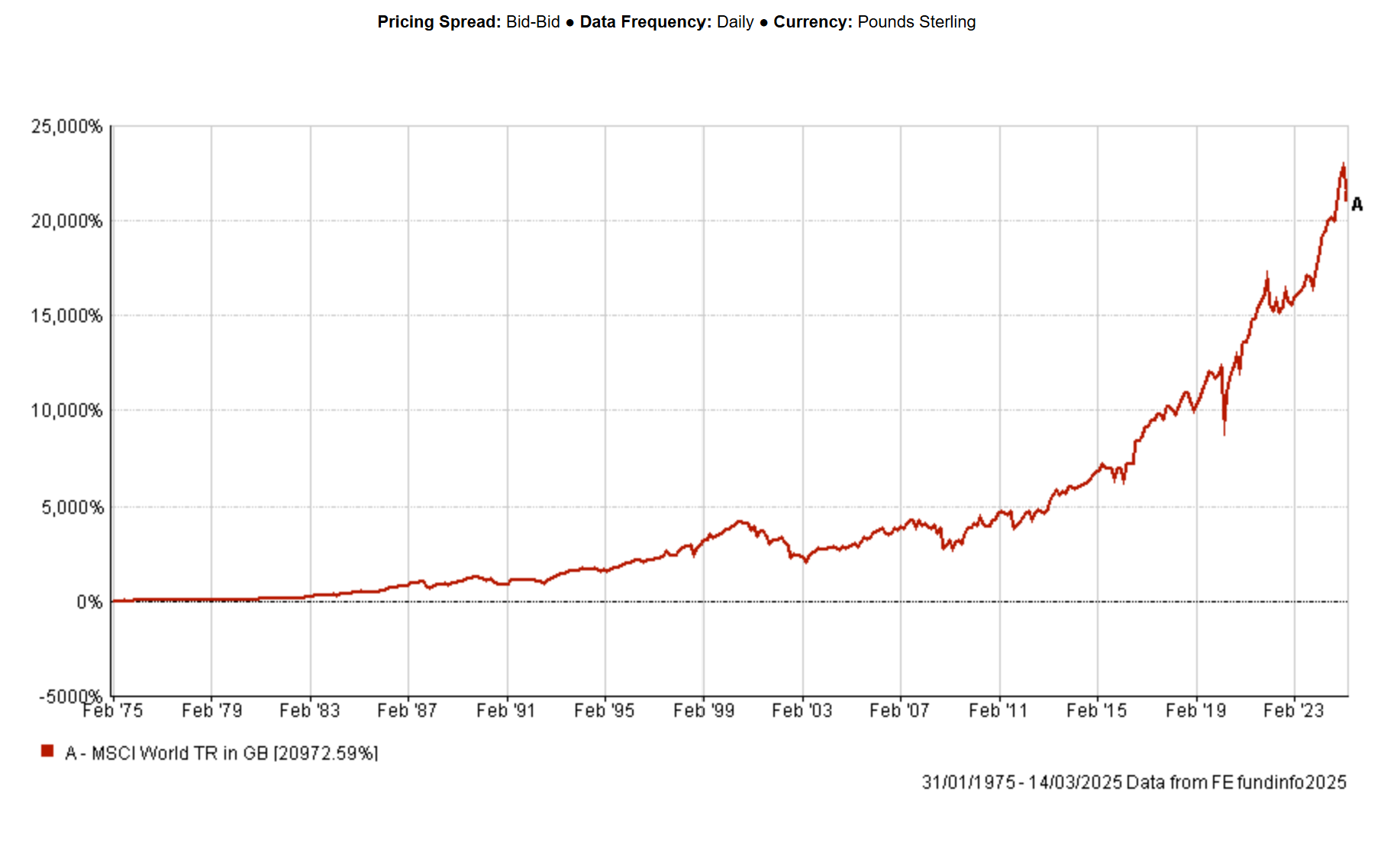

If we look at any long term chart of a successful investment, we see that the magic tends to arrive on the right hand side of the screen.

The point by which returns have built and built upon each other, and maximum compounding kicks in.

But to get to that point, as we know, we need to remain invested. We need to stay in the game.

If you’re bored in the airport and find yourself in WH Smith1 checking out the business book section - you will always find a copy of "Shoe Dog".

It tells the story of Phil Knight, the man who created Nike and is an ode to the grit and determination required to build a global brand.

After Knight set up what was originally “Blue Ribbon Sports” in 1964, the business wasn’t making enough money on its own to support him.

So he spent eight years working three jobs - full-time as an accountant at PWC, teaching accountancy in the evenings at a local college and running his business at night and on the weekends.

Eight years. Working all of the hours that God gave, trying to keep afloat - trying to keep himself in the game and give himself a chance to get to the right hand side of the chart.

In 1980 Nike went public and today the “swoosh” is arguably the most recognisable logo on the planet.

As for Mr Knight, he is currently estimated to be worth in and around $45 billion, depending on what day of the week it is.

In the early days, I am sure there were times when he questioned whether it was all worth it. But something must have compelled him to bite down on his gumshield and persevere.

Little wins. Hope.

The best definition of “diversification” I have ever heard is that if you are properly diversified you will always be disappointed by something in your portfolio. If everything in your portfolio is working at any given time, you just aren’t diversified enough.

We have seen in the past that there are a couple of benefits to being properly diversified.

First of all, risk management - when you have enough of a spread every unsuccessful investment has less impact on the overall pot.

Secondly, being properly diversified ensures that you will be in those few extreme winners of tomorrow that drive overall market returns.

But there is another, more subtle benefit. Being diversified asks less of you as an investor.

I’ll show you what I mean.

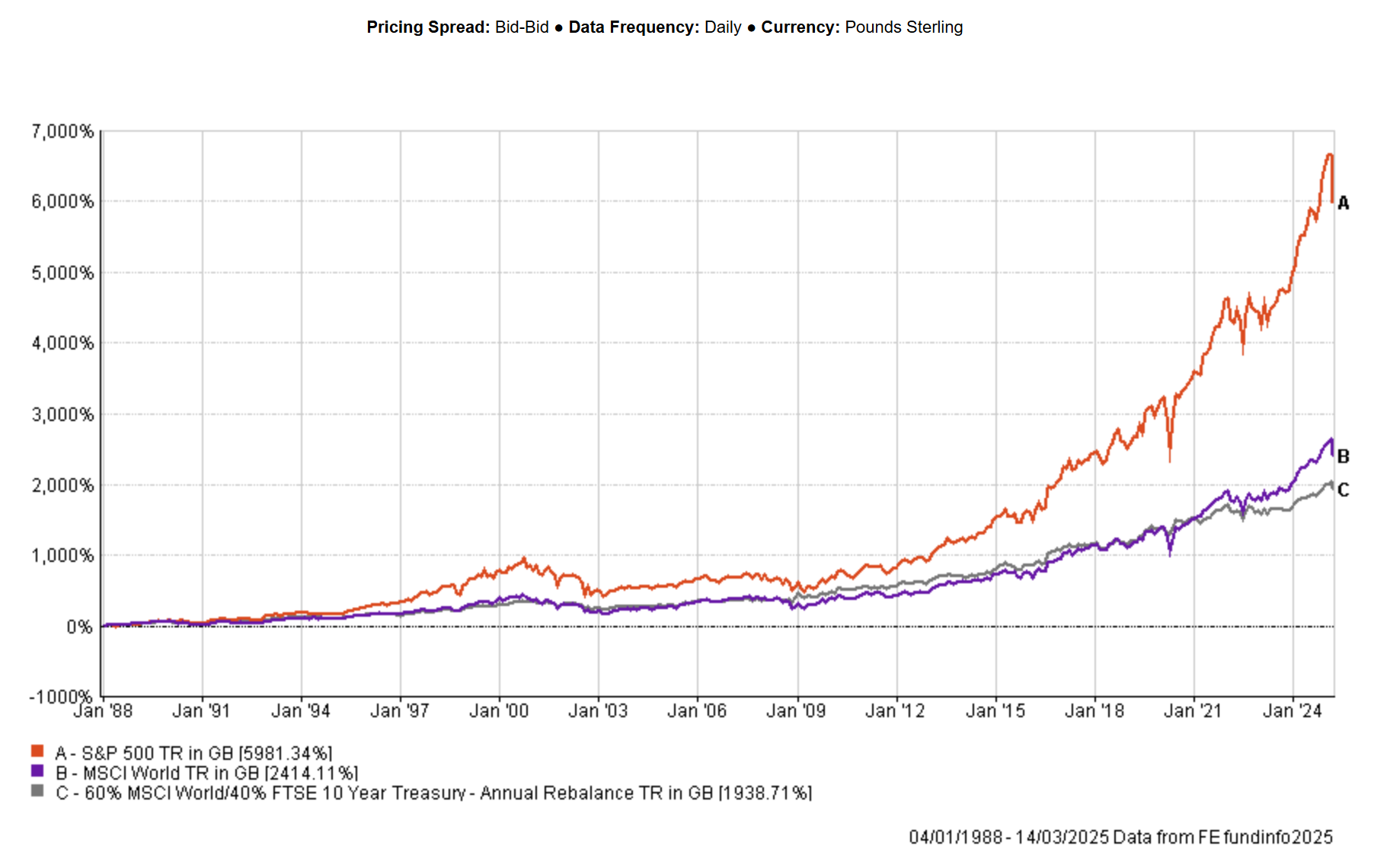

The below chart shows the performance of the S&P 500 (the American stock market), the MSCI World Index (the global stock market) and a simple global 60% stock & 40% bond portfolio2 - from the start of 1988 until today.

“I’ll take the S&P 500 please Carol”.

Of course you would. But almost forty years ago you couldn’t possibly have known that the S&P was going to destroy every other major market in advance. More to the point, you couldn’t possibly have known it at every stage along the journey either.

I have reviewed the monthly returns generated by each of the three strategies above, and the table below shows how frequently each portfolio generated a positive return over five, seven and ten years.

What we see is the more diversified strategies provide more consistent performance.

Although we know today that the S&P would have been the knockout investment - in order to get that return you had to sit tight during several ten year periods where you lost money.

Now, I don’t know everything about investing - far from it.

But I do know people, and I am telling you that the modern investor absolutely does not have the patience/fortitude/ignorance to stick with something after ten years of it not working. We get pissed off if the Deliveroo man is running a bit late.

We need our portfolios to offer up hope frequently enough for it to feel bearable to stick with them. To get ourselves to the right hand side of the chart.

The 60/40 portfolio in particular did just this3. There were no seven or ten year periods, during the timeframe analysed, where it generated a negative return. The 60/40 investor saw signs of life there more frequently.

As Mr Nelson’s original post points out, the figures begin to look even better when we incorporate tilts towards so called “investment factors” - but that feels like a tale for another time.

My main point is this. The perfect investment strategy is the one that you can stick with. For most people this will require a significant degree of diversification.

But not everyone. This is an inherently personal thing. You might believe that picking individual shares or trading in and out of markets represents your path to investment success. I wouldn’t agree with you based on my experience, but good luck to you.

What really matters isn’t finding the strategy that performs the best in a “back test”. It is having enough faith in your chosen approach that you will be able to persist when every fibre of your being is screaming “too much, not for me this”.

Whatever you need to get to the right hand side.

Have a great weekend.

Past performance is not indicative of future returns. None of the above is intended to constitute advice to any individual. If you have any queries regarding your individual situation, then please consult a regulated financial adviser.

Other book shops are available.

60% MSCI World/40% FTSE Treasury Index, rebalanced annually.

I would love to see the same numbers for the MSCI ACWI Index, which includes Emerging Markets (MSCI World is only developed markets really). The data that I had available for the MSCI ACWI didn’t go back far enough.

I would be willing to bet that the numbers for the MSCI ACWI look better than for the MSCI World, due to the higher levels of diversification and the run that Emerging Markets went on during the first decade of the 2000’s when US markets were struggling.