The "Everything Else" Rally

Fan of a chart sir? Step right up.

On Thursday 31st October at 1 o’clock I will be running a lunchtime webinar covering the fallout from the Budget and the main planning opportunities that I see off the back of it.

If the latest reports are to be believed, the most anticipated Budget for ages could be a bit of a damp squib. If this proves to be the case, register here for no other reason than watching me flounder trying to fill half an hour of #content.

Via @PortfolioMeta on X - a historically low number of individual stocks within the S&P 500 (the US stock market) have outperformed the index year to date.

The first takeaway from the above (to my small mind at least) is that in most years, the majority of stocks underperform their index.

Therefore if you are in the business of trying to beat an index by investing in individual names, the numbers tell us that you won’t necessarily have the wind at your back.

It is also easy to forget sometimes, I certainly do, that the stock market isn’t just this abstract number. It is, quite literally, a “market of stocks”. And over the past couple of years, the overall return of this market has been carried by just a handful of companies.

As a consequence of this narrow performance, the proportion of the total US market that is held within the largest companies has been only going in one direction. Stock market “concentration” has been on the rise.

This isn’t just a US phenomenon either.

At first blush, this all sounds like a bad thing. If all of the performance in a given market is coming from only a handful of names - surely that is inherently dangerous?

That is certainly what is implied by the first chart I shared above. The last time that the performance of the US market was driven by so few individual stocks was just before the “Dot Com Crash”.

An overly concentrated stock market being an unhealthy one is certainly a neat story, and one that makes intuitive sense. It’s certainly a narrative that is happily pushed by the usual Doomsday merchants.

Just a shame then that it is total nonsense. The US market has actually done better in the past when concentration has been on the rise.

Things need not go badly from here either. Instead of the largest stocks in the index beginning to fall and bringing down the market with them, the rest of the market can catch up and outperform.

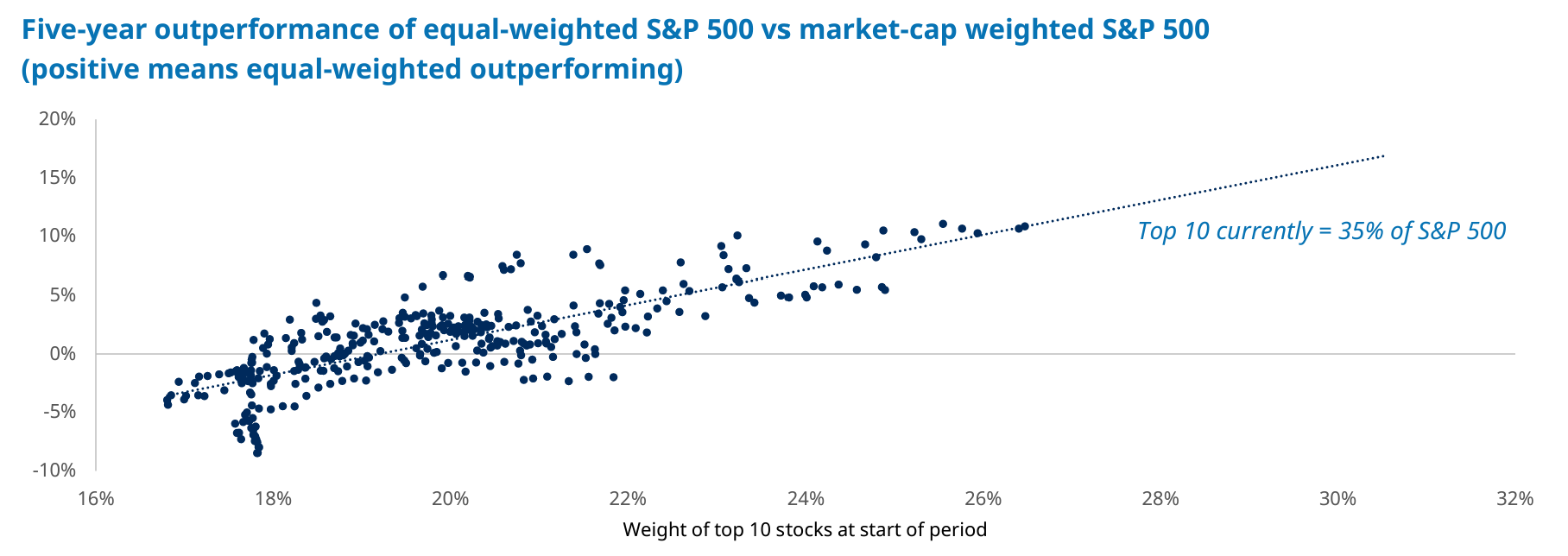

This is exactly what we have (mostly) seen in the past. The below (excellent) chart from Schroders shows that following periods of high market concentration, a simple “equal weighted” strategy will usually outperform the “market cap weighted” index equivalent1.

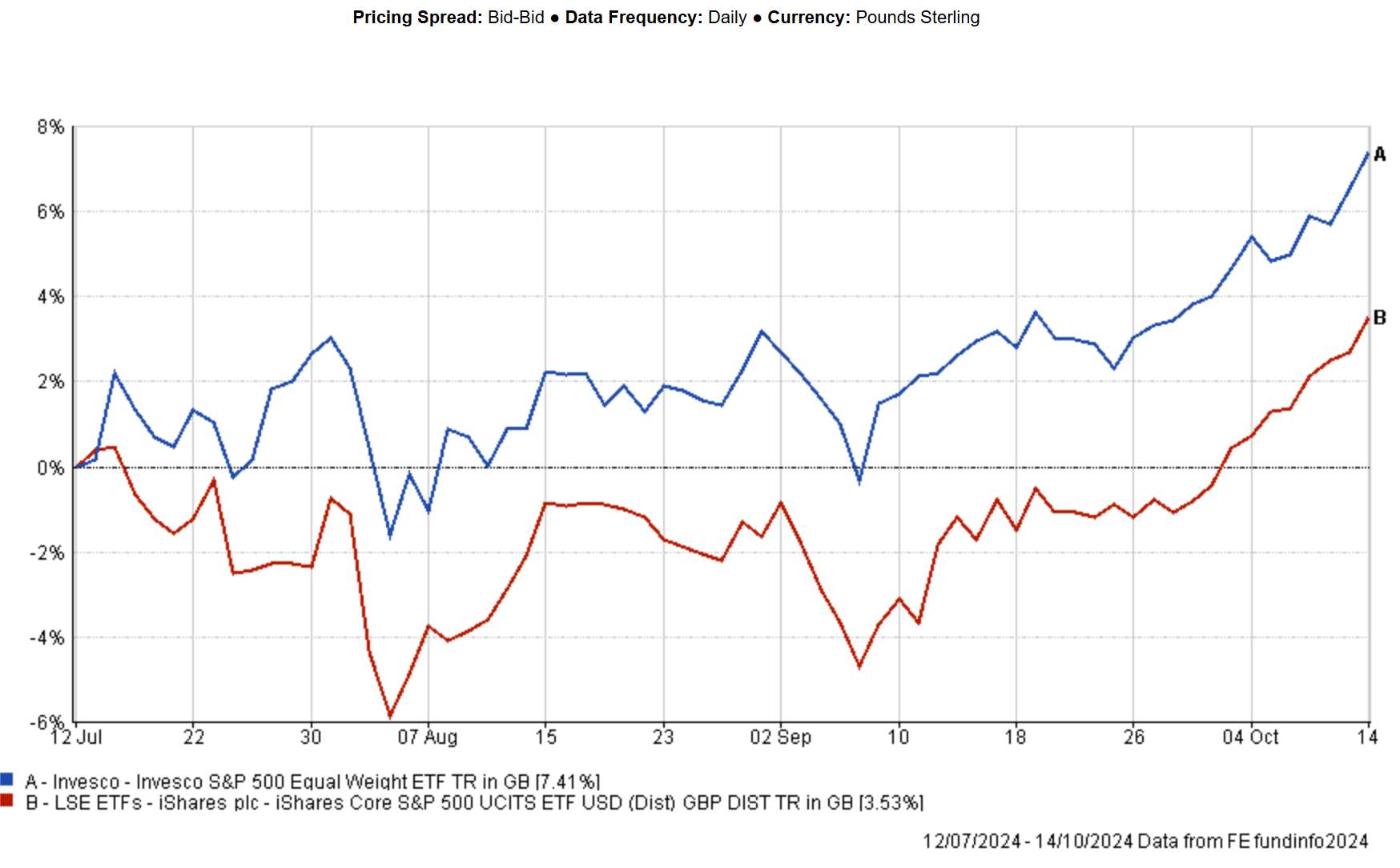

Whisper it quietly, but there are signs that history could be repeating. The below (less excellent) chart shows the performance of an S&P 500 Equal Weighted Index versus the regular S&P over the last three months.

A couple of swallows don’t make a summer, and there have been plenty of false starts for smaller companies over the past few years, but there is definitely a world where market concentration reverts towards the mean without everything falling out of bed. Where performance comes from “everything else” rather than the biggest names.

I know it’s been quite technical this week, but my broad point is this.

There are lots of people out there that spin narratives to suit themselves. Everyone’s selling something.

Quite a lot of the time, these narratives can make a lot of intuitive sense too.

But the devil is almost always in the detail. Either ignore the spin, or do the digging.

Have a great weekend.

Past performance is not indicative of future returns. None of the above constitutes advice to any individual.

Most of the major stock market indices globally are calculated on a “market cap weighted” basis. That is to say that the performance of the largest companies are given the most weight in calculating the performance of the index, and vice versa.

An “equal weight” index, as the name suggests, differs by giving all of the component stocks within the index the same weighting when calculating performance.

Comparing these two indices provides us with a relatively simple method of comparing whether the largest companies within an index are outperforming the smaller ones.